Analysis

Wages Up 46%. Rent Up 105%. The Data Behind Ireland's Housing Crisis.

Since 2014, rents have more than doubled and property prices have surged by 113%. Wages? They've risen just 46%. At this rate, a generation of Irish workers will never own a home.

Statire Research

28 March 2026 · 6 min read

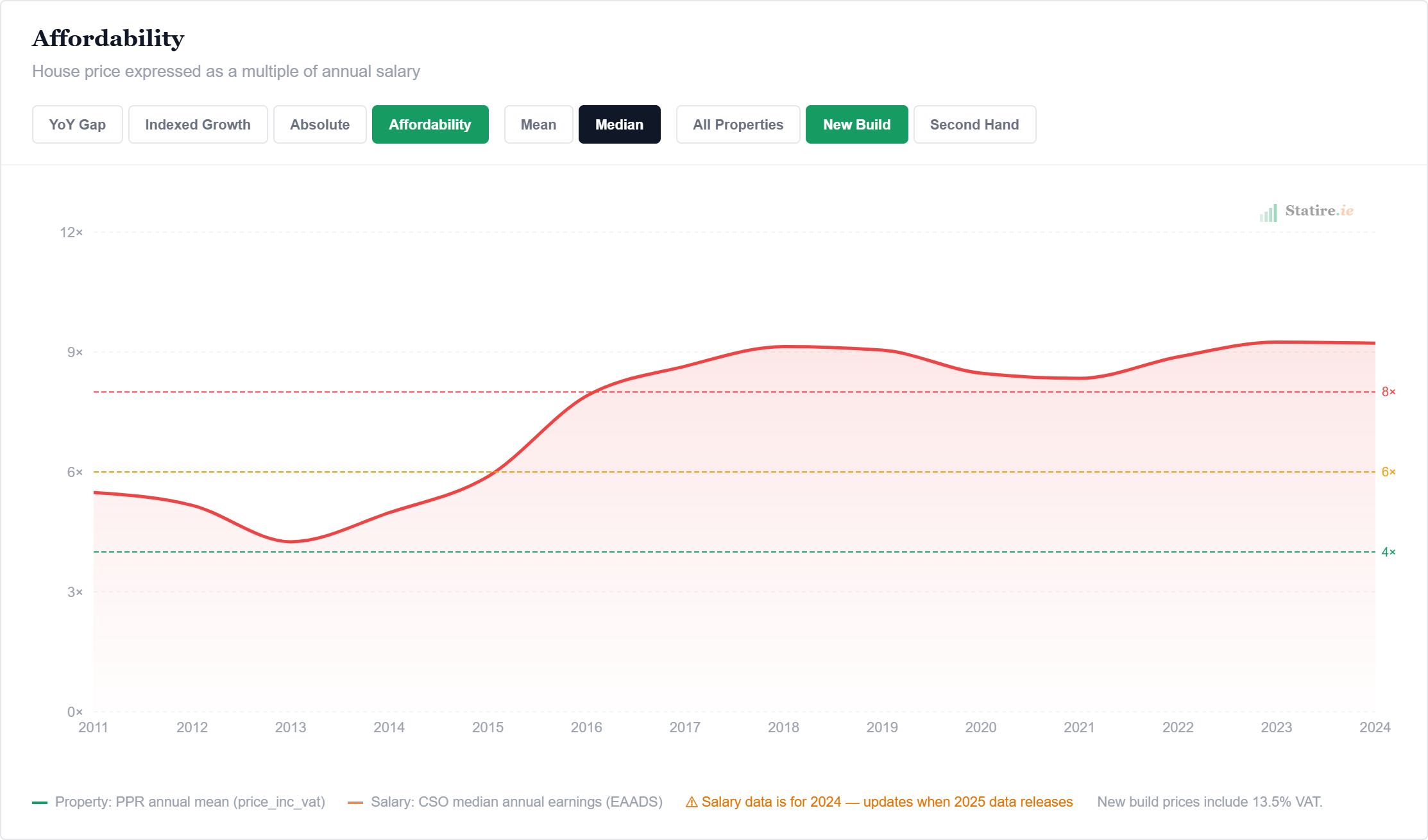

There is a number that should alarm every worker in Ireland: 9.2.

That is how many years of the average gross salary it now takes to buy a median new-build home. Not to save up comfortably. Not while paying rent. Just the raw, pre-tax salary divided into the purchase price. In 2013, it was 4.3.

House price as a multiple of annual salary. Source: PPR and CSO EAADS. Explore interactive version →

The affordability data on Statire lays it out starkly. But affordability is only one side of the story. The deeper question is: why are wages failing to keep pace?

The growth gap

We tracked three metrics since 2014: average annual earnings, average annual rent, and average property sale prices. We indexed their growth side by side. The result is sobering.

Wages have grown at roughly 3–5% per year over the past decade. That sounds healthy until you realise that rents have been climbing at 7–9% and property prices at 6–11% in the same period. Compounded over twelve years, the gap is enormous. A worker in 2014 earning around €36,000 now earns roughly €53,000. But the rent they were paying, €843 a month back then, has ballooned to €1,732.

Year by year, the gap widens

Looking at the year-on-year percentage change paints an even clearer picture. In almost every single year since 2014, both rent and property price growth have outpaced wage growth. The only exception was 2020, when the pandemic temporarily suppressed housing costs. Even then, wages actually rose that year too, partly due to compositional effects as lower-paid jobs disappeared first.

In 2022, the gap was at its most extreme: property prices surged 11.5% while wages grew just 3.4%. Rent climbed 5.8% the same year. By 2023, rents had accelerated further to 9.2% annual growth, the highest in five years, as the landlord exodus picked up pace. An estimated 42,300 rental properties were lost between 2020 and early 2025 as private landlords quit the market.

Rent is eating your salary

The internationally recognised threshold for housing affordability is spending no more than 30% of gross income on rent. Ireland crossed that line at a national level in 2015 and has never looked back.

In 2014, the average Irish worker spent about 28% of their gross annual income on rent. By 2025, that figure had climbed to nearly 40%. In Dublin, where a one-bed now costs roughly €2,500 a month, the picture is far bleaker. The SCSI has found that only the top 20% of earners can now afford to rent an average apartment in the capital.

And it is not just rent. If you are trying to save for a deposit while paying market rent, the maths are brutal. Assuming a 10% deposit on the average property and saving 20% of what remains after rent, it now takes 7.3 years to save enough. In 2014, it was 4.2 years. For a new-build, where the affordability multiple has now hit 9.2 times annual salary, the wait is longer still.

It is not just housing

Housing is the biggest line item, but it is far from the only one squeezing Irish workers. The broader cost of living has risen sharply across the board, and wages have struggled to keep pace with any of it.

Food prices surged by over 12% in 2022 and 2023 alone, driven by supply chain disruption and the war in Ukraine. While inflation has since eased, prices have not come back down. A weekly shop that cost €100 in 2020 now costs closer to €125. Essentials like dairy, bread, and meat have all seen double-digit increases that are now baked into baseline prices.

Energy costs tell a similar story. Electricity prices for Irish households remain among the highest in Europe, even after the worst of the 2022 energy crisis passed. At the peak, average annual electricity bills exceeded €2,500, more than double what they were in 2020. Government credits and falling wholesale gas prices have helped, but household bills remain well above pre-pandemic levels. Home heating oil, which over 600,000 Irish homes depend on, saw prices spike above €1,500 per fill during the crisis. It has come down, but remains volatile and tied to global oil markets that no Irish policy can control.

Motor fuel has followed a similar pattern. Petrol and diesel prices hit record highs in 2022 and, while they have eased, remain elevated. For commuters outside Dublin with limited public transport options, the car is not a luxury. It is a necessity that now costs significantly more to run.

The cumulative effect of all this is brutal. Even if your rent stayed flat and your wages kept pace with inflation, the rising cost of food, energy, and transport means your disposable income is being eroded from every direction. For renters in particular, who are already spending 40% of their income on housing, there is almost nothing left to absorb these increases. Saving for a deposit becomes not just difficult but, for many, genuinely impossible.

Ireland's CPI tracker shows the full picture. The Consumer Price Index has risen roughly 20% since 2020. Wages over the same period are up about 17%. That gap may look small, but when housing costs, which are not fully captured by CPI, are layered on top, the real erosion of purchasing power is stark.

Building more, but still not enough

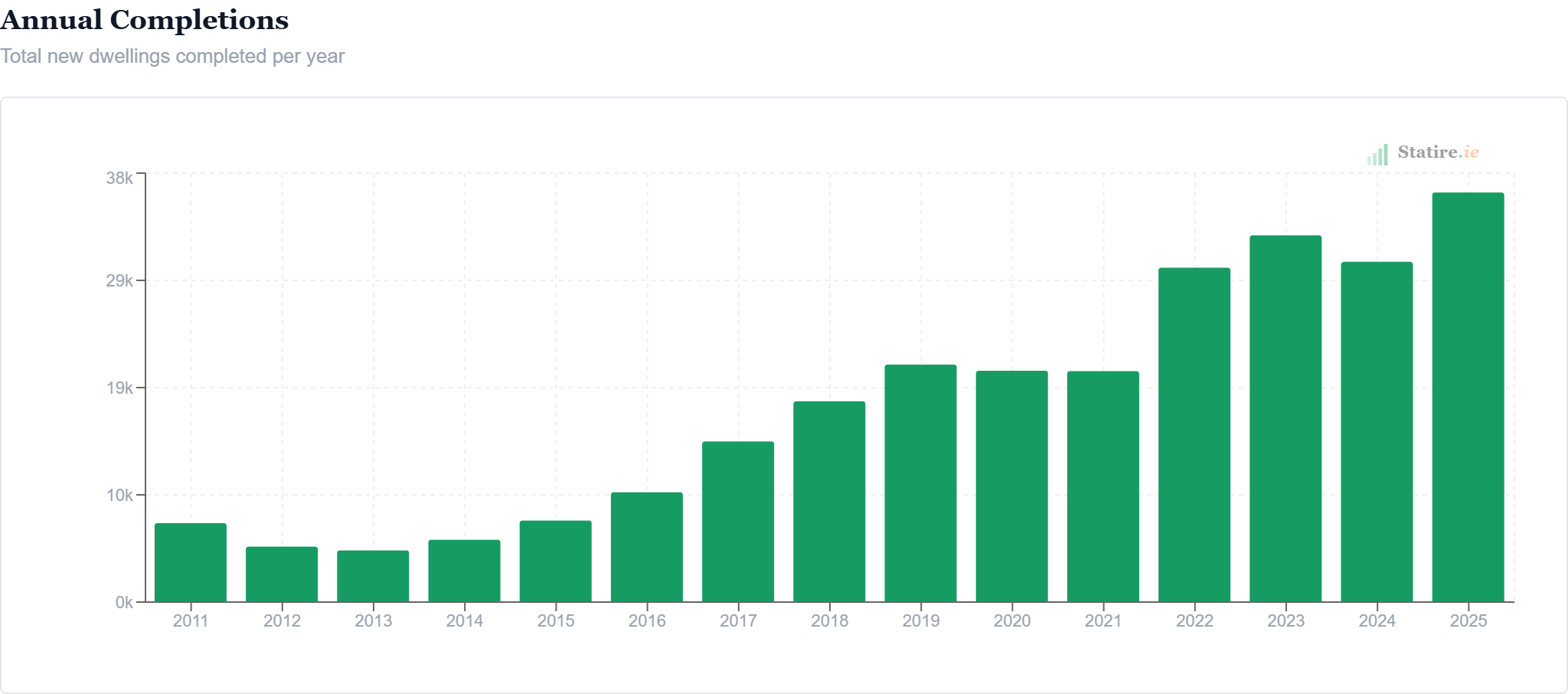

There is a supply-side story too. Ireland completed 36,284 new homes in 2025, the highest figure since CSO records began in 2011, and a 20% jump on 2024. Apartment completions surged nearly 39% to over 12,000 units, now making up a third of all new builds.

But even at this pace, output is falling well short of demand. The Taoiseach has acknowledged that 50,000 homes per year are needed, sustained for a decade, to close the gap. At current completion rates, Ireland is delivering roughly 70% of what is required. The government has quietly abandoned annual targets in favour of a cumulative 300,000 homes by 2030, a figure most analysts consider optimistic.

Annual housing completions. Source: CSO. Explore interactive version →

The planning pipeline is also a concern. Housing starts in key Dublin local authority areas dropped dramatically in 2025, with planning permissions falling to under 35,000 units nationally. Today's planning shortfall is tomorrow's supply crisis.

A crack in the market?

There are early signs that something is shifting. Property prices in the first quarter of 2026 have shown the slowest rate of growth since late 2023. In Dublin, transaction prices actually fell 1.1% in Q1, marking the second consecutive quarterly decline.

Is it the beginning of a correction? Perhaps. The consensus among analysts is that stretched affordability itself is now acting as a natural cap. But there may be other forces at play. Global trade uncertainty, driven by escalating tariff tensions, has rattled investor sentiment across Europe. Ireland, with its outsized dependence on US multinationals like Apple, Google, Meta and Pfizer, is uniquely exposed. These firms account for roughly 10% of all private employment and pay a third of all wages nationally.

Then there is the AI question. The tech sector that has fuelled Dublin's premium housing demand is undergoing rapid restructuring. As AI reduces headcounts across the industry, the knock-on effects on housing demand, particularly at the top end of the market, could be significant. Over 90% of senior property professionals have cited global instability as a primary concern for 2026.

None of this means a crash is imminent. Ireland's fundamental undersupply problem remains, and the economy is still forecast to grow 3% this year. But the cocktail of unaffordability, global uncertainty, and a tech sector in flux means the market is more fragile than at any point since the pandemic.

Explore every property sale in Ireland

Statire's interactive Property Price Register lets you search all recorded sales by address, county, price range and date — updated weekly, fully searchable.

What happens next

The trajectory is unsustainable. If property and rent costs continue to outpace wages at anything close to the current rate, homeownership for the average Irish worker will become mathematically impossible within the next decade. Among 25–34 year olds, ownership has already collapsed from 68% in 1991 to 27%.

One-third of Irish people are now considering emigration due to housing costs, the second-highest rate in the EU. That is not a housing market with a problem. That is a country with a crisis.

The data is clear. Wages are not keeping up. They have not kept up for over a decade. And unless something fundamental changes, whether in supply, in policy, or in the broader economic environment, they never will.

Data sources: CSO Earnings, Hours & Employment Costs Survey (EHECS); RTB Rent Index; Property Price Register; CSO New Dwelling Completions. All charts and data are available on Statire.ie. Data updates automatically as new figures are published.