Property Analysis

Ireland's housing market is at an inflection point, and AI is now the bigger question than supply

Q1 2026 completions hit the highest level in over a decade, but mortgage approvals, corporation tax receipts and the first AI-driven multinational layoffs in Dublin all point to an Irish housing market approaching a turning point.

Statire

23 May 2026 · 9 min read

Irish builders completed 7,856 new homes in the first quarter of 2026, a 32.9% increase on the same quarter a year earlier and the strongest opening quarter the country has recorded since the financial crisis. After more than a decade in which supply was framed as the central problem in the Irish housing market, the construction response is finally arriving in volume.

The question is whether buyers will be there to absorb it.

New dwelling completions per quarter, Q2 2016 to Q1 2026. Source: CSO NDQ06. View live supply pipeline data →

The affordability gap is now structural

The standard reading of Irish house prices has been that prices keep rising because not enough homes are being built. That reading is becoming harder to sustain. Even as completions accelerate, the underlying ratio between household incomes and house prices has stretched to levels that would historically have triggered a correction in any open economy.

According to CSO and Property Price Register data, the median Irish house price reached €383,000 in May 2026, while median annual earnings sit at €44,816. That is a price-to-salary multiple of 7.6 times. The long-term Irish norm is closer to four times, and most European peer economies cluster between four and six times.

The shape of the divergence matters more than any single ratio. Salaries grew roughly 28% between 2017 and 2024. House prices grew 75% over the same window, and rents climbed nearly 60%. The wedge between what households earn and what they pay to live in a house, whether buying or renting, has rarely been wider in modern Irish history.

Cumulative growth in salaries, house prices and rents, 2017 to 2026. Source: CSO EAADS, PPR, RTB Rent Index. View live affordability metrics →

This is the gap that demand-side state supports have been working to fill. Help to Buy provides a tax refund of up to €30,000. The First Home Scheme contributes up to 30% of the purchase price as a state equity share. The Local Authority Home Loan offers below-market lending to applicants refused elsewhere. Without these supports, the affordability ceiling at four times gross income would mechanically cap a single first-time buyer on median earnings at around €180,000 of borrowing capacity, against a national median price more than double that.

Wondering what a property is actually worth in today's market?

Use Statire's valuation tool to get a free comparable-based estimate.

The new variable: artificial intelligence

What has changed in the past twelve months is the credibility of the assumption that Irish wages will keep rising fast enough to support the current price level. The first explicit AI-driven layoffs at a major Irish multinational employer arrived on 20 May 2026, when Meta confirmed 350 redundancies at its Dublin operations as part of an 8,000-strong global cut. Chief executive Mark Zuckerberg framed the change as a shift to AI-first operations, saying that projects which previously required large teams could now be carried out by “a single very talented person.”

The announcement came on top of an existing 40% reduction in Meta's Irish workforce from a post-Covid peak of around 3,000. Taoiseach Micheál Martin acknowledged on the day of the announcement that “there is certainly an AI trend beginning.” Tánaiste Simon Harris went further, warning that “there could be significant upheaval in the jobs market over the next decade, and it could be earlier rather than later in that decade.”

Meta is not the only signal. Accenture announced 11,000 global redundancies in late 2025 under an explicitly AI-driven restructuring programme, with chief executive Julie Sweet warning that staff who could not adapt would be “exited.” Accenture is among the largest private sector employers in Ireland. The Indian IT services firms that staff much of the contractor base for Dublin tech multinationals, including Wipro, TCS and Infosys, are reporting revenue growth at less than half their historical rates.

Wider data from Stanford's Digital Economy Lab suggests that software developer employment for workers aged 22 to 25 in the United States fell by roughly 20% from its late 2022 peak by July 2025, while employment for those over 30 in the same AI-exposed roles grew between 6% and 12%. Indeed Hiring Lab reports junior tech postings down 34% over five years against senior postings down 19%. The labour market story is not yet a story of mass tech unemployment. It is a story of a hollowed-out middle and a narrowing entry point.

For Dublin, the marginal buyer of a city home over the last decade has been a mid-career professional in a US-headquartered multinational paying global tech wages into a small Irish labour pool. That cohort is precisely where AI is now compressing fastest.

What the chain is already showing

Headline transaction prices are still positive, but the second-hand market is already signalling stress. The Banking and Payments Federation Ireland reported 565 mover-purchase mortgage approvals in January 2026, the lowest monthly count since June 2020. Mover approvals are arguably the cleanest test of unsubsidised affordability available, because movers are constrained to a 3.5 times income borrowing cap and cannot avail of Help to Buy or First Home Scheme top-ups.

Asking price inflation has now decelerated for five consecutive quarters. Bank of Ireland's Q1 2026 property report shows Dublin asking price inflation at 2.9% year-on-year, the softest reading in almost three years and down from 8.4% at the end of 2024. The premium paid over asking price has narrowed from 8.5% during the 2025 summer peak to 6.5% in February 2026, suggesting bidding intensity is fading even where stock is still scarce.

Year-on-year change in median second-hand house prices, 2011 to 2026. The 2026 bar is the lowest positive print since 2020. Source: Statire analysis of PPR. View live price momentum data →

The fiscal channel that gets overlooked

The state has spent the past three years backstopping affordability through a layered first-time buyer support stack. Help to Buy, the First Home Scheme, expanded Local Authority Home Loan limits, the Vacant Property Refurbishment Grant and the Starter Homes Programme together amount to one of the most aggressive demand-side housing interventions in any developed economy. These measures have effectively become the floor under Dublin prices in the €400,000 to €500,000 segment, where they intersect with the four-times-income borrowing limit.

That floor is funded from corporation tax. The Irish Fiscal Advisory Council reported in February that 46% of all corporation tax in 2024 came from just three companies, broadly understood to be Apple, Microsoft and Eli Lilly. Q1 2026 corporation tax receipts came in 3.1% below the same period a year earlier when one-off Apple-related payments are excluded. The Central Bank's March 2026 Quarterly Bulletin warned explicitly of “medium-term negative risks” if US companies begin to curtail their Irish operations.

The mechanism is straightforward. When corporation tax rises, the government can afford to expand demand-side housing subsidies. When corporation tax falls, that capacity narrows. The Q1 2026 data is the first sign in several years that the corporation tax cycle may have turned, at exactly the moment AI-driven multinational restructuring becomes visible.

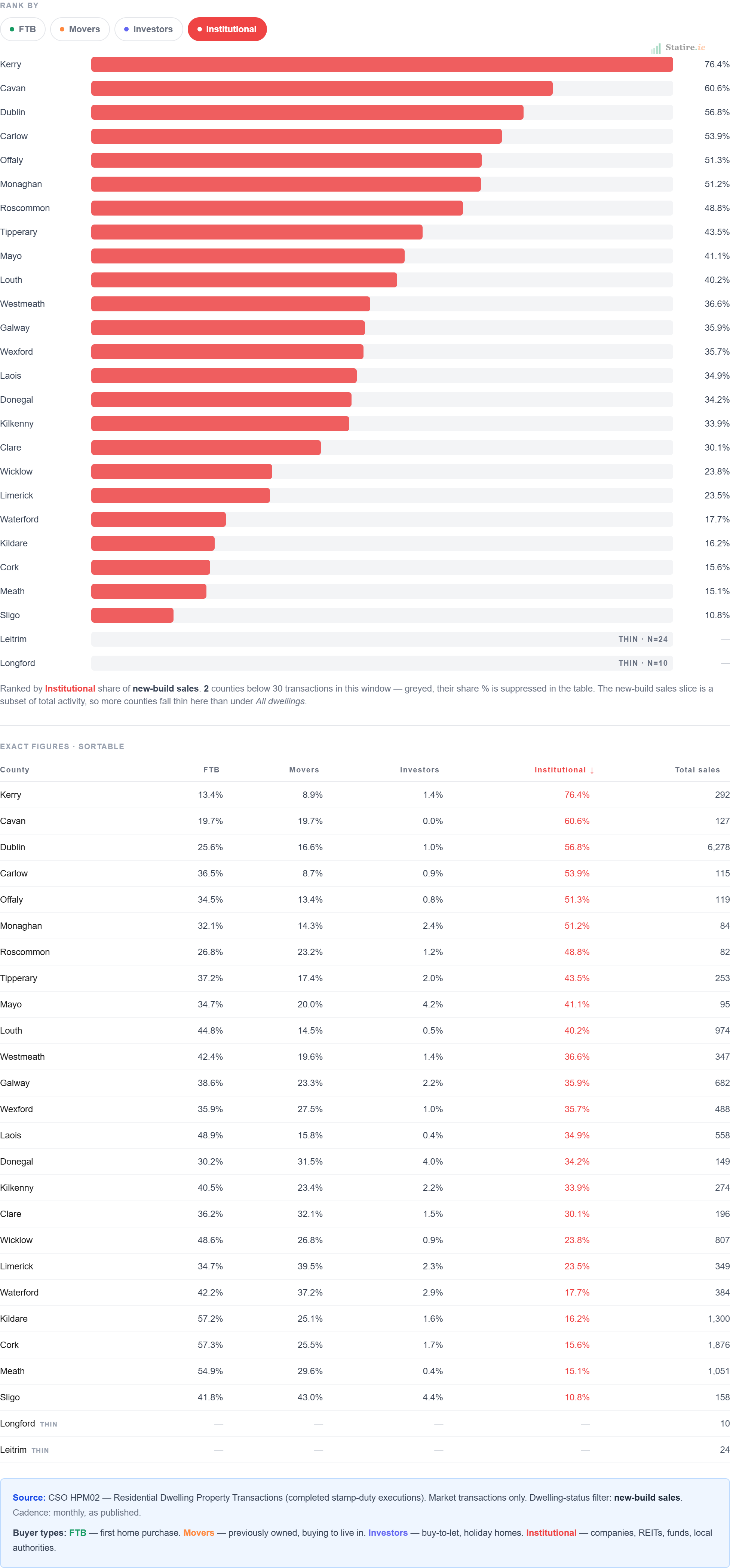

Where new supply is actually going

There is a further wrinkle in the supply story that complicates the narrative of relief. Of the 7,298 new homes purchased in Dublin in 2025, 56% were acquired by “non-household entities” rather than individual buyers, according to CSO data reported by The University Times in April 2026. A substantial portion of that, 3,448 units, was acquired by Dublin local authorities for social housing. The remainder went principally to private institutional investors active in the build-to-rent sector.

CBRE's 2026 Ireland real estate outlook described the private rented sector as “the market to watch” and forecast that institutional investment volumes in residential property would more than double in 2026, with JLL projecting total real estate investment of between €3.5bn and €4bn for the year. The implication is that a meaningful share of new completions enters the rental market rather than the ownership market. New supply competes for renters rather than relieving the buyer demand that has been driving prices.

Institutional and fund share of new-build property purchases by county. Source: CSO HPM02, Statire analysis. View live cross-county buyer breakdown →

For first-time buyers, this means the headline completion number overstates the supply actually arriving in the segment of the market they can access. The increase in private dwellings on the open market is real but considerably smaller than the topline 32.9% suggests.

The international canary

Other small, open, US-multinational-exposed economies are already showing the pattern that may emerge in Ireland. Singapore reported Q1 2026 private home price growth of 0.3% on the quarter, the weakest reading since the contraction of Q3 2024, with landed property prices falling 1.8%. The Singapore government has responded by releasing roughly 50% more new housing supply than its ten-year average. Multiple Singapore-based multinationals announced layoffs in early 2026, citing AI-related restructuring across tech, manufacturing and professional services.

Singapore is typically six to twelve months ahead of Ireland on the same cycle because of its more flexible labour market and faster price discovery. What is happening there now is what may begin showing in Irish transaction data in late 2026 or 2027. Israel, the third small economy heavily exposed to US tech, has plateaued rather than fallen, but its housing market is structurally supported by a 200,000-unit supply deficit that is much larger than Ireland's.

Where the market actually sits

Looking at where transactions cluster gives a sharper picture than the headline median. In Dublin, the largest single price band over the last two years is €400,000 to €500,000, accounting for over 9,500 transactions out of 37,926. Nationally, the densest band is €300,000 to €400,000.

Distribution of Dublin property sales by price band, last 24 months. 37,926 transactions analysed. Source: Statire analysis of PPR. View live price distribution data →

These are the segments most exposed to a marginal household income shock. They sit precisely at the dual-income or single high-earner affordability ceiling under the Central Bank's loan-to-income rules. The €400,000 to €500,000 Dublin band is largely dependent on a buyer earning at least €100,000 (4 times income on a maximum stretch) or a household combining two earners on €120,000 to €130,000 in total. Both profiles are concentrated in multinational tech, multinational pharma, professional services and senior public sector roles. The first two are now visibly under AI-related pressure. The third is downstream of the first two through advisory, audit, legal and consulting work.

Where this leaves the market

Headline price inflation is still positive. Q1 2026 RPPI growth was 5.7% nationally. Supply is responding. Bank of Ireland still forecasts 4% national house price growth for full-year 2026. None of the data presented here suggests an imminent crash, and Ireland's structural housing shortage remains real even after the recent completion uplift.

But the leading indicators are flashing more clearly than at any point since 2007. Mover purchase mortgage approvals are at five-year lows. Asking price inflation has decelerated for five consecutive quarters. Corporation tax has turned. Net migration fell 25% year-on-year in the most recent CSO release, with emigration to Australia at its highest level since 2013. The first AI-driven Dublin layoffs at a major multinational employer have arrived, and the political response from both the Taoiseach and the Tánaiste acknowledges this is the beginning of a trend rather than a one-off event.

The honest reading is that the next twelve to eighteen months will reveal whether the demand-side supports built up since 2022 can absorb a US multinational income shock that is now visibly underway. Headline nominal price falls are unlikely in 2026 because of the lag between transactions and reported data. Real-terms declines, when measured against the roughly 2% inflation rate, are already plausible by year-end. The question that will define the Irish property market for the rest of the decade is whether AI-driven labour market changes compress the pool of capable buyers fast enough to break what supply alone could not.

For households deciding when to buy, sell or sit, the relevant data is no longer in the headline RPPI release. It is in the monthly BPFI mortgage approvals report, the monthly Exchequer corporation tax returns, the next CSO migration release in August, and whether any other US multinational in Dublin follows Meta in citing AI as the cause of redundancies. Those four series will tell the story before the property page does.

Track the Irish property market with live data.

Explore Statire's full property intelligence platform.

Data sources: CSO NDQ06 (New Dwelling Completions); CSO HPM02 (Residential Dwelling Property Transactions); Property Price Register; CSO EAADS (Earnings); RTB Rent Index; BPFI Mortgage Approvals; Central Bank Q1 2026 Quarterly Bulletin; Bank of Ireland Q1 2026 Property Report; Irish Fiscal Advisory Council; CBRE 2026 Ireland Outlook; JLL Investment Forecast; Stanford Digital Economy Lab; Indeed Hiring Lab; The University Times. All charts and live data are available on Statire.ie.